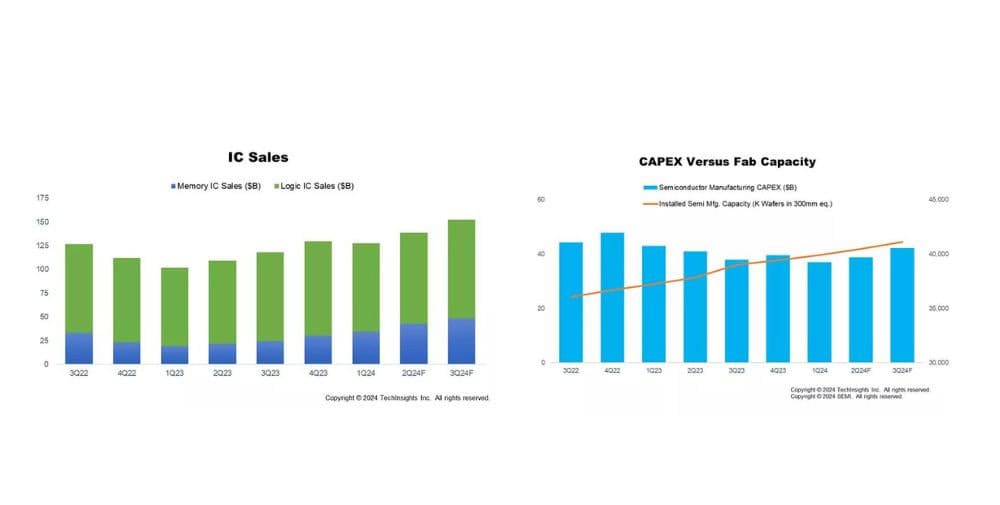

Seasonal fluctuations and weaker-than-expected consumer demand impacted electronics sales in the first half of 2024, resulting in a year-on-year decline of 0.8%. From the third quarter of 2024, electronics sales are expected to rebound, increasing by 4% year-on-year and by 9% compared to the second quarter of 2024. IC sales recorded robust year-on-year growth of 27% in Q2 2024 and are expected to increase by 29% in Q3 2024, surpassing the record levels of 2021, as AI-driven demand continues to boost IC sales growth. Improved demand also led to a 2.6% decline in IC inventories in the first half of 2024.

Installed wafer fab capacity reached 40.5 million wafers per quarter (in 300mm wafer equivalents) in the second quarter of 2024 and is expected to increase by 1.6% in the third quarter of 2024. Foundry and logic capacity grew by 2.0% in Q2 2024 and is expected to increase by 1.9% in Q3 2024 due to the build-up of capacity for advanced nodes. Storage capacity increased by 0.7% in Q2 2024 and is expected to grow by 1.1% in Q3 2024, supported by strong demand for HBM and an improvement in storage pricing conditions. All regions surveyed recorded an increase in installed capacity in Q2 2024, with China remaining the fastest growing region despite mediocre factory utilization rates.

Semiconductor capital expenditure remained conservative in the first half of 2024, resulting in a year-on-year decline of 9.8%. The trend is expected to turn positive from the third quarter of 2024 in response to growing demand for AI chips and the rapid adoption of HBM, with memory capex leading the growth at 16% quarter-on-quarter, while non-memory capex is up 6% quarter-on-quarter.

“Despite moderate semiconductor capex spending in the first half of the year, we expect a positive trend to begin in Q3 2024, led by memory CapEx,” said Clark Tseng, Senior Director of Market Intelligence at SEMI. “Strong demand for AI chips and high-bandwidth memory is driving results across various segments of the semiconductor manufacturing ecosystem.”

“The entire semiconductor supply chain is rebounding this year as the market prepares for a surge in 2025,” said Boris Metodiev, Director of Market Analysis at TechInsights. “AI will certainly continue to drive high-quality ICs to the market while supporting investment for AI chip capacity expansion and HBM in particular. As consumer demand recovers and new technologies such as AI are marginalized, unit volumes and more importantly revenues will recover and support the broader semiconductor manufacturing sector.”

The Semiconductor Manufacturing Monitor (SMM) report provides comprehensive data on the global semiconductor manufacturing industry. The report highlights key trends based on industry indicators, including capital equipment, manufacturing capacity, and semiconductor and electronics sales, and includes a forecast for the capital equipment market. The SMM report also includes two years of quarterly data and a quarterly outlook for the semiconductor manufacturing supply chain, including leading IDM, fabless, foundry and OSAT companies. An SMM subscription includes quarterly reports.

About SEMI

SEMI ® is the global industry association connecting more than 3,000 member companies and 1.5 million professionals worldwide in the semiconductor and electronics design and manufacturing supply chain. We accelerate our members’ collaboration in solving the industry’s greatest challenges through advocacy, workforce development, sustainability, supply chain management and other programs. Our SEMICON® trade shows and events, technology communities, standards and market intelligence help drive business growth for our members and drive innovation in design, devices, equipment, materials, services and software that enable smarter, faster and safer electronics.

– – – – –

Further links

👉 www.semi.org

Graphic: SEMI (www.semi.org) and TechInsights (www.techinsights.com), August 2024